Why is technology critical for construction finance? Key insights from the Payapps UK research report

The construction industry is undergoing a seismic shift, and this is evident in the finance function. The 2026 Payapps UK Research Report – Construction Finance – Why Technology is Critical reveals how finance teams are now at the heart of strategic decision-making, risk management, and supply chain resilience – but are often held back by outdated processes and limited resources.

The evolving role of construction finance

Finance teams in construction are expected to do more than ever: from processing subcontractor payments and managing cashflow to supporting ESG reporting and ensuring compliance with ever-changing regulations. Yet, despite these demands, most teams remain small and heavily reliant on manual processes. The average construction firm manages 210 subcontractors with just five finance staff, creating a mismatch between responsibility and capacity.

The technology gap

The report highlights a significant technology gap. Half of respondents still use spreadsheets, 46% rely on email, and 27% use pen and paper to manage subcontractor payments, whilst only 44% have adopted dedicated payment management software. This reliance on legacy tools leads to errors, bottlenecks, and poor visibility – making it difficult to forecast cashflow, maintain compliance, and avoid costly disputes.

Strategic priorities and challenges for construction finance

Over the next 24 months, finance leaders are prioritising:

- Demonstrating ESG governance (51%)

- Improving process efficiency with technology (45%)

- Enhancing payment times across supply chains (41%)

- Boosting profit margins (41%)

Purpose-built technology can help alleviate these pressures by streamlining workflows and automating repetitive tasks to reduce workload, strengthening compliance and improving visibility – allowing finance teams to shift their focus from administration to strategic delivery.

The findings support this. In fact, 48% of Payapps users surveyed prioritise improving profit margins over the next 24 months, compared to 37% of non-tech users surveyed. Similarly, 59% of tech users surveyed prioritise ESG governance, compared to 44% of non-tech users. This suggests that digital maturity enables finance teams to contribute more meaningfully to long-term business objectives.

Productivity under strain

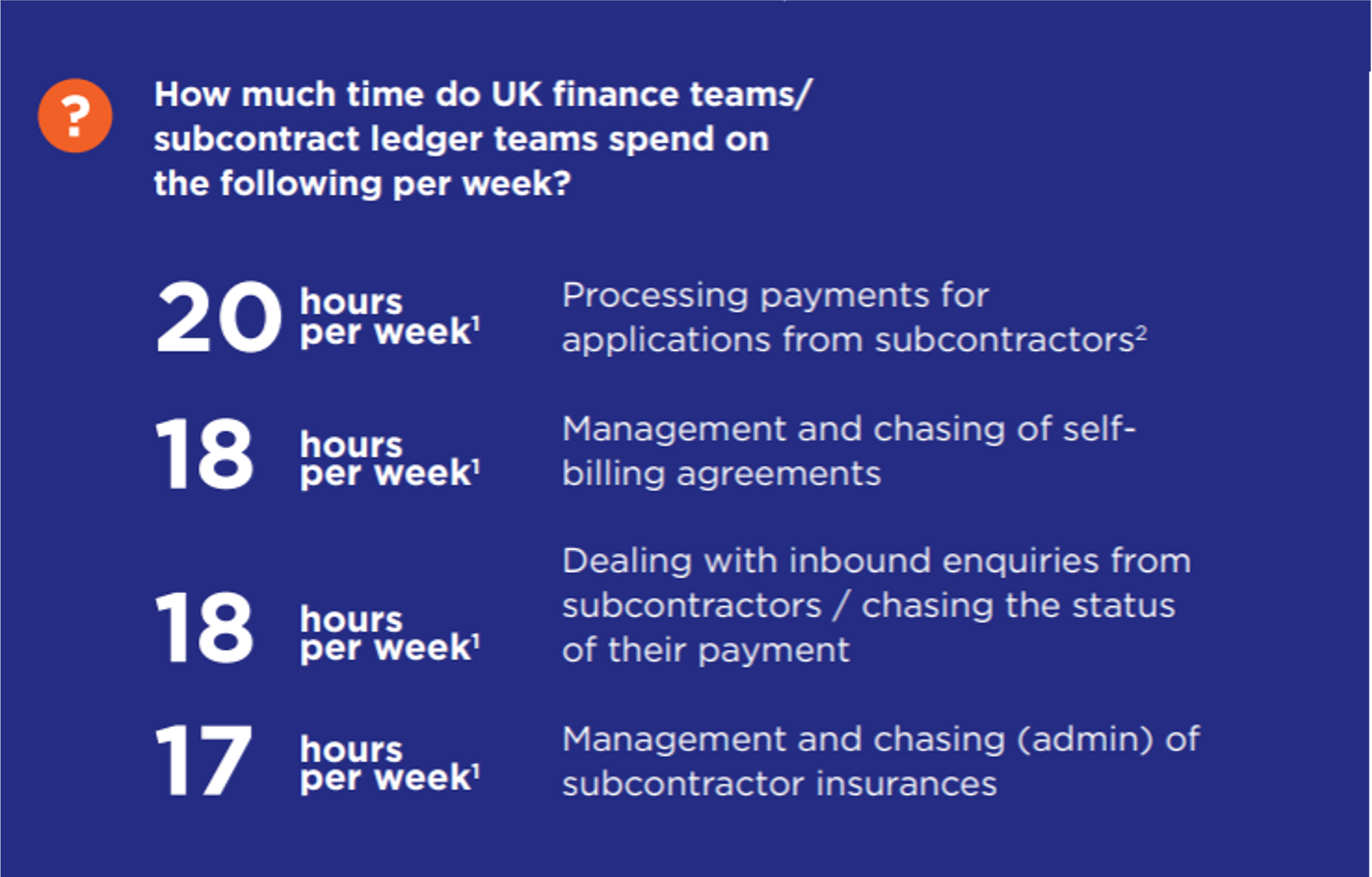

Administrative overload is a major concern. UK finance teams spend an average of 20 hours per week processing payments, with additional time spent on self-billing agreements and managing subcontractor enquiries.

This leaves little room for strategic activities like forecasting and risk analysis. Technology, such as Payapps, can automate these tasks, freeing up time for higher-value work.

Risk, visibility, and compliance

Limited visibility over payment obligations exposes businesses to financial and regulatory risk. Only 20% of respondents have total visibility before payments are approved, and 59% are concerned about cashflow forecasting. Incorrect tax treatment and compliance failures are also common, with 64% worried about the financial implications of ‘smash and grab’ adjudications. Technology improves reporting, compliance, and agility, helping finance teams adapt to regulatory changes.

Supply chain stability

Prompt payment is essential for supply chain resilience. While 98% say paying subcontractors promptly is a priority, execution often falls short. None of the UK organisations surveyed would qualify for a Fair Payment Code award, and delays increase the risk of disputes and insolvencies. Technology enables more accurate, timely payments and strengthens supplier relationships.

Construction payment technology as a catalyst for change

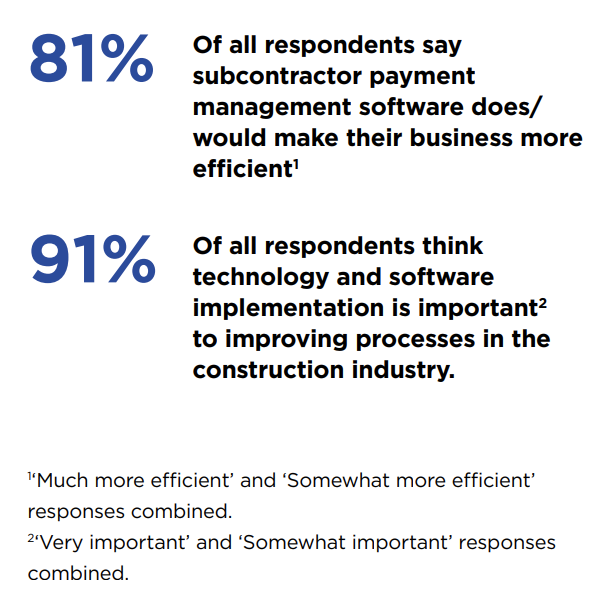

The industry is aligned on the need for digital transformation. 81% believe payment software would make their business more efficient, and 91% see technology as vital for improving construction processes. Among UK companies not yet using dedicated software, 63% plan to introduce it within 6 months. Purpose-built payment management systems are now seen as essential for sustainable growth and financial resilience.

Key takeaways for construction finance leaders

The research highlights a clear shift in both the expectations placed on construction finance teams and the tools required to meet them. Together, they paint a picture of a function at a critical inflection point.

- The role of finance in construction has fundamentally changed – teams are central to protecting margins, managing risk, and supporting ESG governance.

- Responsibility has outpaced capacity, with small teams managing large subcontractor networks.

- Manual and fragmented processes undermine performance and increase risk.

- Administrative overload prevents finance teams from operating strategically.

- Limited visibility directly threatens margins and resilience.

- Payment performance is a critical supply chain risk lever.

- Technology materially improves outcomes.

- Digital transformation is no longer optional.

Ready to future-proof your construction finance function?

Download the full research report to discover how your organisation can leverage technology to build resilience, improve compliance, and drive sustainable growth.